The following is a commentary I received which I thought you would find of interest. I suspect that the information provided will be very interesting for the Devos and Granholm Michigan Governor's race. The numbers ought to worry the Governor.

It certainly makes one wonder as a resident of Windsor what our new Economic Development Commission will do. Probably little, since it has no Executive Director appointed yet. Surprise, surprise.

It was the best of times (Ontario) is was the worst of times (Michigan).

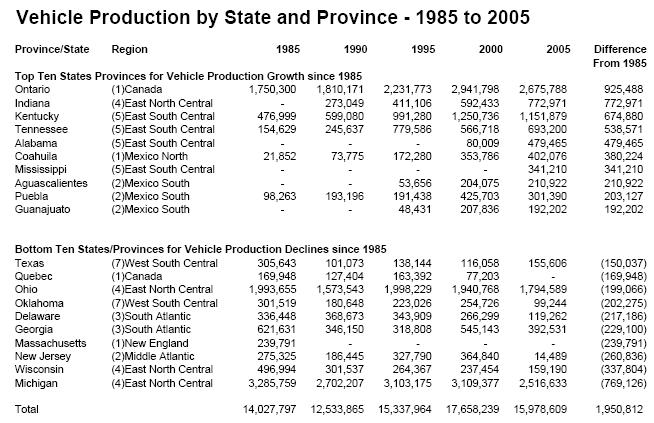

The final vehicle production by State and Province is now available and Ontario maintained a comfortable lead over Michigan as the number one jurisdiction in North America for the production of vehicles. In 2005 Ontario produced 2,675,788 vehicles and Michigan produced 2,516,633 vehicles. Ontario first out produced Michigan in 2004 and grew its lead over Michigan in 2005. We first started tracking production by state and province in 1985 and in that year Michigan produced 3.29 million vehicles compared to Ontario's 1.75 million vehicles. Michigan has lost 769,126 units of production while Ontario has gained 925,488 million units of production.

Michigan has obviously been hurt by the declining fortunes of GM, Ford and DCX and will likely see even more production declines as the current restructuring of these companies play themselves out. In addition, Michigan is highly unionized and has only attracted one new domestic producer (Mazda - Flat Rock) while Ontario has four new domestic plants (Honda -2, Toyota and CAMI) and is about to see a fifth when Toyota opens next year). Ontario also spent most of the last two decades aggressive promoting investments with the Japanese and welcoming them into our province while Michigan politicians, at all levels of Government, spent most of the last two decades fighting (bad mouthing would be a better phrase to use) the import nameplate companies arguing for quota's, tariffs etc and in general being negative to any and all import nameplates. A good friend of mine in the development community has always said that "Business goes where it is wanted and stays where it is appreciated". From that perspective, Michigan could learn a lesson from Ontario and Alabama and Kentucky and Mississippi and Tennessee, etc .. for that matter.

Other top producing areas include Ohio at 1.79 million units, Kentucky and Missouri at 1.15 million units, Indiana at 773 thousand units, Tennessee at 693 thousand units, Alabama at 479 thousand units, Illinois at 455 thousand units and California at 422 thousand units.

I find it very interesting to also look at the change over the last 20 years. Ontario is not only the top producing jurisdiction but also is the number one growth area for vehicle production with production up 925 thousand units. Michigan has seen the largest decline in production, down 769 thousand units. The US South has seen significant increases (Kentucky, Tennessee, Alabama and Mississippi) as well as Mexico (Coahuila, Aguascalientes, Puebla and Guanajuato). But Ontario remains number one in both overall volume and change in volume since 1985 and arguably is the best jurisdiction anywhere in North America for the production of vehicles.

It is going to be tough but Ontario should be able to maintain and possibly grow its production over the next few years. We know that Toyota is adding a significant plant in Cambridge and GM, Ford and DCX have all re-committed to most of their plants in Canada. Honda has two significant plants and is holding its own. And CAMI is finally getting full use of its capacity in Ingersol. There might be some lost production at GM and Ford with their restructurings announced last fall and in January but the Toyota investment should offset these losses. The thing that is impossible to predict is whether the vehicles we produce in Ontario will continue to strike a chord with consumers. In some respects, Ontario's spectacular production performance has been related as much to the vehicle mix produced in Canada as to the investment commitment from the various OEMs. There is no reason to believe that this won't continue but you never know. We have very little exposure to the fastest declining market segments in North America (large and luxury SUV's) but we have fairly high exposure to mid sized vehicles (mini vans and intermediate cars). All these segments are under siege at consumers move down market to entry level vehicles and up market to luxury products. We also have high exposure to pick up trucks. The commercial use side of this market should be solid but the personal use side of the pick up truck market is soft.

I believe our vehicle production position is as much related to the market as it is to investment commitments and the cost of doing business in Canada versus the US or Mexico. This will tell the tale over the next few years.

It certainly makes one wonder as a resident of Windsor what our new Economic Development Commission will do. Probably little, since it has no Executive Director appointed yet. Surprise, surprise.

It was the best of times (Ontario) is was the worst of times (Michigan).

The final vehicle production by State and Province is now available and Ontario maintained a comfortable lead over Michigan as the number one jurisdiction in North America for the production of vehicles. In 2005 Ontario produced 2,675,788 vehicles and Michigan produced 2,516,633 vehicles. Ontario first out produced Michigan in 2004 and grew its lead over Michigan in 2005. We first started tracking production by state and province in 1985 and in that year Michigan produced 3.29 million vehicles compared to Ontario's 1.75 million vehicles. Michigan has lost 769,126 units of production while Ontario has gained 925,488 million units of production.

Michigan has obviously been hurt by the declining fortunes of GM, Ford and DCX and will likely see even more production declines as the current restructuring of these companies play themselves out. In addition, Michigan is highly unionized and has only attracted one new domestic producer (Mazda - Flat Rock) while Ontario has four new domestic plants (Honda -2, Toyota and CAMI) and is about to see a fifth when Toyota opens next year). Ontario also spent most of the last two decades aggressive promoting investments with the Japanese and welcoming them into our province while Michigan politicians, at all levels of Government, spent most of the last two decades fighting (bad mouthing would be a better phrase to use) the import nameplate companies arguing for quota's, tariffs etc and in general being negative to any and all import nameplates. A good friend of mine in the development community has always said that "Business goes where it is wanted and stays where it is appreciated". From that perspective, Michigan could learn a lesson from Ontario and Alabama and Kentucky and Mississippi and Tennessee, etc .. for that matter.

Other top producing areas include Ohio at 1.79 million units, Kentucky and Missouri at 1.15 million units, Indiana at 773 thousand units, Tennessee at 693 thousand units, Alabama at 479 thousand units, Illinois at 455 thousand units and California at 422 thousand units.

I find it very interesting to also look at the change over the last 20 years. Ontario is not only the top producing jurisdiction but also is the number one growth area for vehicle production with production up 925 thousand units. Michigan has seen the largest decline in production, down 769 thousand units. The US South has seen significant increases (Kentucky, Tennessee, Alabama and Mississippi) as well as Mexico (Coahuila, Aguascalientes, Puebla and Guanajuato). But Ontario remains number one in both overall volume and change in volume since 1985 and arguably is the best jurisdiction anywhere in North America for the production of vehicles.

It is going to be tough but Ontario should be able to maintain and possibly grow its production over the next few years. We know that Toyota is adding a significant plant in Cambridge and GM, Ford and DCX have all re-committed to most of their plants in Canada. Honda has two significant plants and is holding its own. And CAMI is finally getting full use of its capacity in Ingersol. There might be some lost production at GM and Ford with their restructurings announced last fall and in January but the Toyota investment should offset these losses. The thing that is impossible to predict is whether the vehicles we produce in Ontario will continue to strike a chord with consumers. In some respects, Ontario's spectacular production performance has been related as much to the vehicle mix produced in Canada as to the investment commitment from the various OEMs. There is no reason to believe that this won't continue but you never know. We have very little exposure to the fastest declining market segments in North America (large and luxury SUV's) but we have fairly high exposure to mid sized vehicles (mini vans and intermediate cars). All these segments are under siege at consumers move down market to entry level vehicles and up market to luxury products. We also have high exposure to pick up trucks. The commercial use side of this market should be solid but the personal use side of the pick up truck market is soft.

I believe our vehicle production position is as much related to the market as it is to investment commitments and the cost of doing business in Canada versus the US or Mexico. This will tell the tale over the next few years.

No comments:

Post a Comment